Professional Judgment and Professional Skepticism Is There a Difference Explain

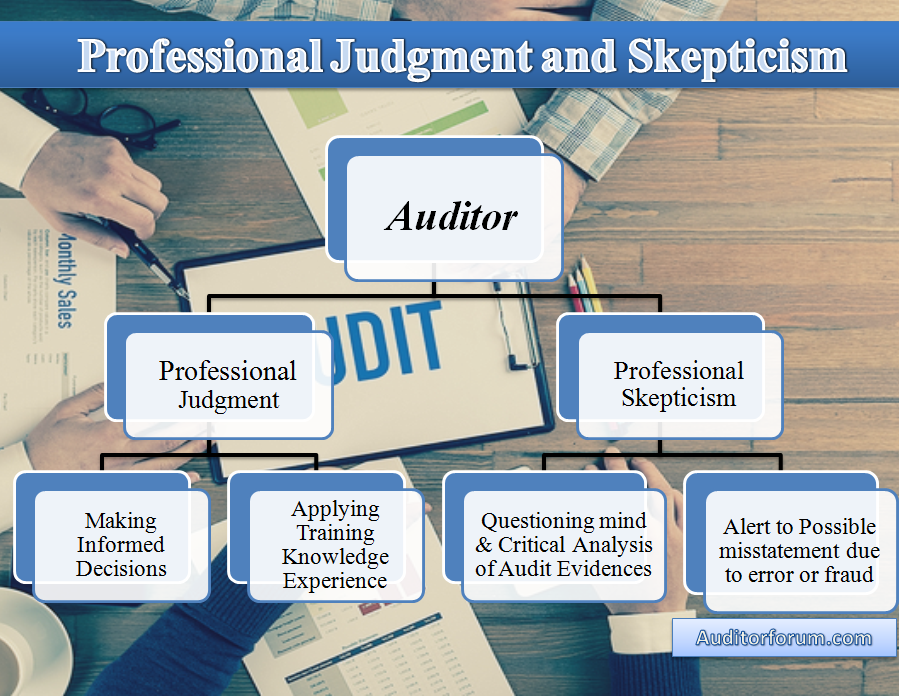

It is an attitude of professional which include questioning mind alertness in conditions which may indicate possible misstatement due to fraud or error. Where professional skepticism is the attitude of having an inquisitive mind and having to question audit evidence intuitively for its sufficiency and appropriateness professional judgment is the application of your knowledge skills and training regarding auditing and accounting to make informed decisions and deciding how to respond to particular situations during the audit.

3 Elements Of Professional Skepticism Aci Learning

Professional skepticism is especially important in the areas affected by managements judgment and decisions.

. PROFESSIONAL SKEPTICISM Professional skepticism is having a questioning attitude critically assessing evidence obtained and. Refer to the Auditing in Practice feature. This lesson discusses the concept of professional skepticism and professional judgment including personal bias and other impediments in the performance of audit and non-audit engagements.

In our discussion of the KPMG professional judgment framework we pointed out that biased judgments can be made because of judgment tendencies. The concept of professional judgment is considered including its theoretical foundations how it is developed and how it may be assessed. Evidence that is separate and apart from the process of.

Professional judgment is central to providing. To them when exercising professional judgment in the context of applying the conceptual framework. It means making informed decisions by a professional accountant about the courses of actions that are appropriate in the circumstances during an audit engagement in the context of auditing accounting and ethical standards and by applying the relevant training.

It is not enough for the auditor to have an appropri-ate process to identify the issues and to. Professional Judgement and Professional Skepticism. The proper exercise of professional judgment requires the auditor to reach a correct conclusion.

This concept includes skepticism in the usual sense an inquiring mind and a critical eye towards audit evidence. When is there sufficient evidence. Professional Skepticism and Professional JudgmentProposed Texts Mark-up from ED 2 All comment letters can be accessed on the.

Professional skepticism may not be necessary for the critical assessment of evidence. It is important to document procedures completed considerations taken into account and conclusions reached that required professional judgment in the working paper file. Explain the need to plan and perform audits with an attitude of professional scepticism and to exercise professional judgment.

Naturally management has an expected outcome in these areas and it is crucial that auditors apply both a. Professional judgment and skepticism. Nature timing and extent of the specific procedures professional judgment may be involved.

Frames help us make sense of things but they also make it difficult for us to see other views The mindset of a professional auditor is one of objectivity and professional skepticism. Professional skepticism is crucial to your duty of care as an auditor. Professional skepticism is an attitude that includes.

The accountants expertise and experience areown sufficient to reach a conclusion. Auditors and audit firms need to remember that their. In the Task Forces view there are no significant matters raised by the respondents that have not been brought to the Boards attention.

Professionals are asked to engage in complex and unpredictable tasks on societys behalf and in doing so must exercise their discretion making judgments--decide what is best in the particular situation rather than what is right in some. Define professional skepticism and explain its importance in an audit. Some areas potentially affected by managements judgement include related-party transactions and financing transactions.

Or whether There is a need to consult with others with relevant expertise or experience. A questioning mind and a critical assessment of. When planning and performing an audit the auditor should adopt an attitude of professional scepticism.

The professional standards define professional skepticism as an attitude that includes a questioning mind being alert to conditions that may indicate possible misstatement due to fraud or error and a critical assessment of audit evidence Given this definition one quickly realizes that professional skepticism cant be easily measured. Acting with proper skepticism allows you to diligently audit in. The committee further explained.

Professional judgment should be documented. Professional skepticism is an attitude that includes a. For example doctors and patients tend to select riskier treatment options when a condition is framed in terms of the odds of dying than when the identical situation is framed in terms of.

One such tendency that was not included in the framework is self-serving bias. In professional practice judgement involves a purposeful and systematic thinking process that. Shall be defined as judgement that is informed by professional knowledge of curriculum expectations context evidence of learning methods of instruction and assessment and the criteria and standards that indicate success in student learning.

Professional Skepticism and Professional JudgmentProposed Texts Mark-up from ED IESBA MeetingDecember 2017 Agenda Item 4-A Page 4 of 4. Appropriately questioning managements perspective by viewing the. The phrases Use your professional judgment She exercised professional judgment or In my professional judgment come up frequently in dietetic practice.

Professional skepticism is an important component of objectivity and essential ingredient for gathering the evidences which are necessary to support audit judgment. Professional skepticism is an attitude which includes questioning the mind and being alert to conditions that may indicate the possible misstatement because of error or fraud and an important assessment of evidence in professional standards the framework for auditor objectivity and professional skepticism is reflected. So in line with the working groups view exercise of professional judgement is never suspended in AUP engagements while its limited in the context of professional competence and due care.

The concept of professional judgment is used in College standards of professional practice guidelines and other resources. Application material to explain how compliance with the fundamental principles in the Code supports. Professional Skepticism and Professional Judgment.

Multiple judgment frames enhance an auditors professional skepticism because better judgments can be made from considering the fact that other frames exist. Questioning mind and a critical assessment of audit. Different points of view.

Need for Further Consultation. IESBA CAG Meeting September 2017 Agenda Item B. They shape our perspectives and determine the information that we will see as relevant or irrelevant important or unimportant.

Five Ways To Engage Learners In Critical Thinking Critical Thinking Experiential Learning Critical Thinking Skills

Pdf Professional Skepticism In Auditing And Its Characteristics

Professional Judgment And Professional Skepticism In Auditing

Randy Clark 436 When Employees Make Mistakes Podcast Marketing Podcasts Business Training Leadership Training

2

Professional Skepticism And Professional Judgment In Auditing Auditing And Attestation Cpa Exam Youtube

2

Empower Kids For Life Natural Logical Consequences Logical Consequences Love And Logic Logic

Professional Judgment And Professional Skepticism In Auditing

2

6 Most Critical Hr Skills And Competencies Skills Communication Skills Employee Relations

Randy Clark 436 When Employees Make Mistakes Podcast Marketing Podcasts Business Training Leadership Training

Rejection A Root In Many Issues Rejection Understanding Emotions Bible Study Notebook

2

Difference Between Absolutism And Scepticism Difference Between

Magazine Mindful Mindfulness Yoga Meditation Meditation Practices

5c21 5 Key Skills For 21st Century Education Computational Thinking Critical Thinking Skills 21st Century Skills

Live By The 4 Agreements The Four Agreements Words Effective Leadership

How To Think Smart Critical Thinking Activities Critical Thinking Critical Thinking Skills

Comments

Post a Comment